I have been experimenting with algorithmic trading for a couple of weeks. Zipline is a Python library for backtesting trading algorithms and I would like to share one of the algorithms I made.

import talib

from zipline.api import record, order_target, history, add_history

import dateutil

import logging

from zipline.utils.factory import load_from_yahoo

from zipline.finance.slippage import FixedSlippage

from zipline.algorithm import TradingAlgorithm

from zipline.finance import commission

logging.basicConfig(level=logging.DEBUG)

# initialize algorithm

def initialize(context):

logging.debug('enter initialize')

context.set_slippage(FixedSlippage())

context.set_commission(commission.PerTrade(cost=5))

context.LOW_RSI = initialize.low_RSI

context.HIGH_RSI = initialize.high_RSI

context.rsi_window = initialize.rsi_window

add_history(context.rsi_window, '1d', 'price')

context.i = 0

context.invested = False

# default parameters for algorithm

initialize.rsi_window = 15

initialize.low_RSI = 30

initialize.high_RSI = 70

# Will be called on every trade event for the securities you specify.

def handle_data(context, data):

logging.debug('enter handle_data')

context.i += 1

if context.i < context.rsi_window:

return

# get the last RSI value

prices = history(context.rsi_window, '1d', 'price')

sec_rsi = talib.RSI(

prices[context.security].values,

timeperiod=context.rsi_window - 1)

# buy and sell flags

buy = False

sell = False

if sec_rsi[-1] < context.LOW_RSI and not context.invested:

# RSI under 30 indicates oversold, time to buy

order_target(context.security, 1000)

logging.debug('Buying {}'.format(context.security))

context.invested = True

buy = True

elif sec_rsi[-1] > context.HIGH_RSI and context.invested:

# RSI over 70 indicates overbought, sell everything

order_target(context.security, 0)

logging.debug('Selling {}'.format(context.security))

context.invested = False

sell = True

# record data for each time increment

record(secRSI=sec_rsi[-1],

price=data[context.security].price,

buy=buy,

sell=sell)

logging.info(context.portfolio.cash)

def run_algorithm(

security='AAPL',

start_date='20100101',

end_date='20150101',

initial_cash=100000,

rsi_window=15,

low_RSI=30,

high_RSI=70):

logging.debug('run_algorithm begin')

# dates

start = dateutil.parser.parse(start_date)

end = dateutil.parser.parse(end_date)

# get data from yahoo

data = load_from_yahoo(stocks=[security], indexes={}, start=start, end=end)

logging.debug('done loading from yahoo. {} {} {}'.format(

security, start_date, end_date))

# create and run algorithm

algo = TradingAlgorithm(

initialize=initialize,

handle_data=handle_data,

capital_base=initial_cash)

algo.security = security

initialize.low_RSI = low_RSI

initialize.high_RSI = high_RSI

initialize.rsi_window = rsi_window

logging.debug('starting to run algo...')

results = algo.run(data).dropna()

logging.debug('done running algo')

return results

if __name__ == '__main__':

import matplotlib.pyplot as plt

# run algorithm and get results

results = run_algorithm(

security='AAPL',

start_date='20100101',

end_date='20150101',

initial_cash=100000,

rsi_window=15,

low_RSI=30,

high_RSI=70)

# get s&p500 and nasdaq indexes

index_data = load_from_yahoo(

stocks=['^gspc', '^ixic'],

indexes={},

start=results.index[0],

end=results.index[-1])

# portfolio value, stock holdings and S&P 500 index

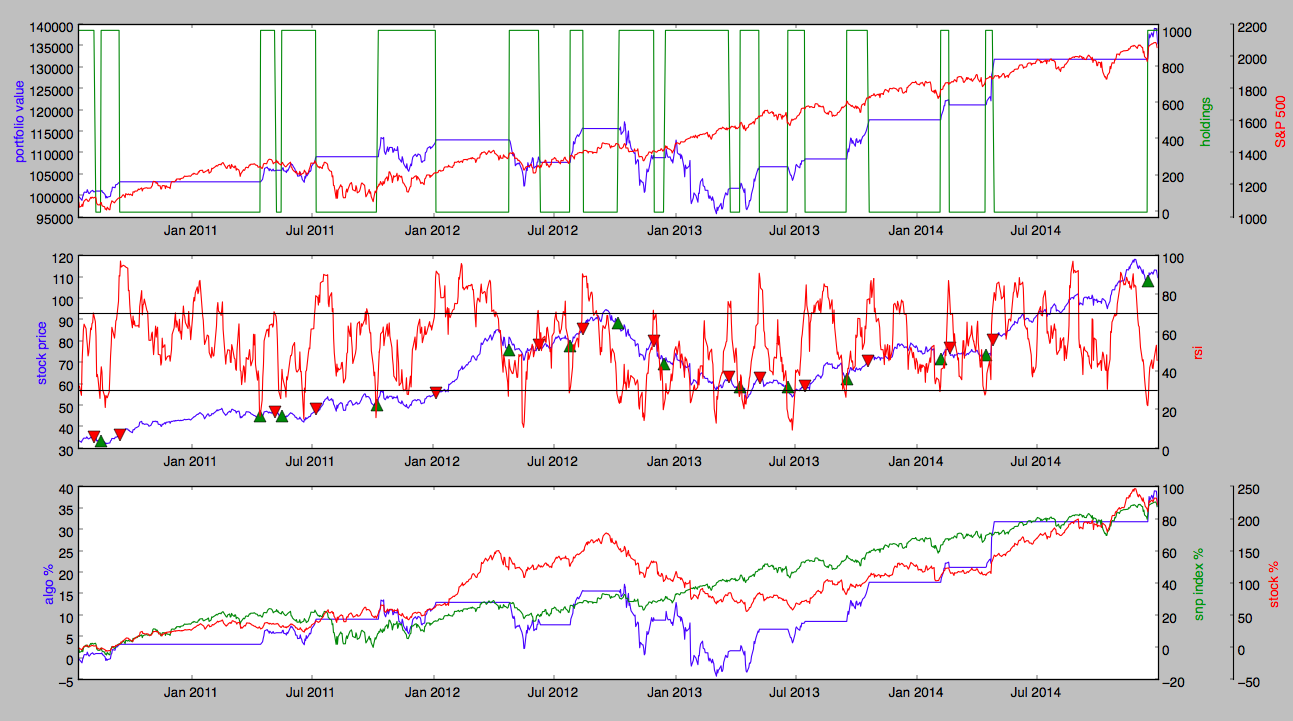

fig = plt.figure(figsize=(12, 6))

ax11 = fig.add_subplot(311)

ax12, ax13 = ax11.twinx(), ax11.twinx()

ax13.spines['right'].set_position(('axes', 1.07))

ax11.set_ylabel('portfolio value', color='blue')

ax12.set_ylabel('holdings', color='green')

ax13.set_ylabel('S&P 500', color='red')

# portfolio value

ax11.plot(results.index, results.portfolio_value, color='blue')

# holdings (number of stocks owned)

holdings = [0 if t == [] else t[0]['amount'] for t in results.positions]

ax12.plot(results.index, holdings, color='green')

ax12.set_ylim([min(holdings) - 30, max(holdings) + 30])

# index

ax13.plot(index_data.index, index_data['^gspc'], color='red')

# algo visualization

ax21 = fig.add_subplot(312)

ax21.set_ylabel('stock price', color='blue')

ax22 = ax21.twinx()

ax22.set_ylabel('rsi', color='red')

# stock

ax21.plot(results.index, results.price, color='blue')

# add sell and buy flags on top of stock price

ax21.plot(

results.ix[results.buy].index,

results.price[results.buy],

'^',

markersize=10,

color='green')

ax21.plot(

results.ix[results.sell].index,

results.price[results.sell],

'v',

markersize=10,

color='red')

# rsi value

ax22.plot(results.index, results.secRSI, color='red')

# add lines to show under- and over value indicator

ax22.plot([results.index[0], results.index[-1]], [30, 30], 'k-')

ax22.plot([results.index[0], results.index[-1]], [70, 70], 'k-')

# portfolio value, stock value and index in percentage

ax31 = fig.add_subplot(313)

ax32, ax33 = ax31.twinx(), ax31.twinx() # share x for other plots

ax31.set_ylabel('algo %', color='blue')

ax32.set_ylabel('snp index %', color='green')

ax33.set_ylabel('stock %', color='red')

ax33.spines['right'].set_position(('axes', 1.07))

# portfolio value

ax31.plot(

results.index,

results.portfolio_value / results.portfolio_value[0] * 100 - 100,

color='blue')

# index

ax32.plot(

index_data.index,

index_data['^gspc'] / index_data['^gspc'][0] * 100 - 100,

color='green')

# stock value

ax33.plot(

results.index,

results.price /

results.price[0] * 100 - 100,

color='red')

plt.show()

If you get it working you should see a plot similar to this one:

If you are observant, it is easy to see that the performance of this algorithm is not good enough to be used on a real portfolio, and it is more of a test.

Links: